The Secrets of The Leader

In many organizations, a common issue is a lack of alignment. Teams feel disconnected, staff members pull in different directions, and communication breaks down. It often feels like no one is truly on the same page. These problems aren’t just accidental, they stem from leadership. And leadership, in my experience, always comes down to values.

Leadership Starts with Daily Actions

Values aren’t just lofty words in a mission statement. They’re what leaders do every single day. Leadership is visible in the small actions: Are you approachable? Are you communicating consistently? Are you prioritizing what matters? Your habits as a leader set the tone for the entire team.

I’ve learned this the hard way. My biggest challenges as a leader have been when I failed to communicate clearly or didn’t act on issues quickly enough. These gaps sent the wrong signals to my team about what was important. Leadership trickles down, and if your actions aren’t aligned with your values, it’s impossible to expect the team to follow suit.

For larger teams, this extends to the management level. Your leadership team must not only align with the values but also live them daily. Leadership is only effective if it’s consistent across every layer of the organization.

The Vision Doesn’t Have to Be Complicated

One mistake many leaders make is overcomplicating their vision and mission. You don’t need an elaborate or abstract statement to lead effectively. Instead, focus on something clear and actionable that drives your team. A good vision gives direction, but it also needs to feel achievable.

Think of leadership like sailing across the ocean. If you’re the captain, it’s not enough to simply say, “We’re going to the other side.” Your team needs milestones: “We’ve crossed 25% of the ocean” or “We’ve passed this island, and here’s what’s next.” These progress markers give people a sense of security and purpose, showing that you’re moving forward together.

Ask What Drives Your Team

Leadership isn’t just about the vision of the organization, it’s also about understanding the motivations of each person on your team. I remember consulting with a company where I asked the management team, “Why don’t you just ask your staff what they really want in life?” They hesitated because they were scared of the answers.

But I don’t think you should fear these conversations. Asking your team what their deep goals are can uncover simple but powerful truths. Maybe someone wants to be home for dinner every night. Maybe someone dreams of traveling more or learning a new skill. Once you know these goals, you can align the company’s objectives with theirs. If there’s a mismatch, it’s better to address it early than let it fester for months or years.

When your team feels like their personal goals are connected to the organization’s vision, you create buy-in. And when you break that vision down into daily and weekly actions, you make progress tangible and motivating.

Three Questions for Reflection

- What values are you living out daily, and how do they align with the culture you want to create?

- When was the last time you asked your team members about their personal goals, and how are you helping them achieve those goals?

- Does your vision feel achievable and actionable to your team? What daily or weekly milestones can you use to track progress?

You Are The Architect – Build What You Want

I want to share a story that I heard once and can’t seem to forget. It’s about a father and his daughter at the playground. The little girl is on the swings, smiling as her dad gently pushes her higher and higher. Then, as the sun starts to set, the dad says, “We need to go home now, sweetheart.” The girl, with the innocence and charm only a child can muster, looks up and says, “Please, Daddy, one more time.”

The dad pauses for a moment and replies, “Okay, one more time.”

Nearby, another parent, visibly stressed and rushing to get home, overhears this exchange. Frustrated, they walk up to the patient father and say, “How do you have so much patience? I just get so frustrated. We’re late for dinner, and I can’t deal with all the delays.”

The father looks at them with quiet understanding and says, “Well, I would do anything to swing my oldest son one more time. But after the accident, he’s no longer with us. So, every time one of my kids asks for ‘one more time,’ I do everything I can to make it possible. I guess you grow a different kind of patience.”

This story always stops me in my tracks. Sometimes we move so fast we don’t realise how grateful we should be. Often the most precious things in life are often unmeasurable and we don’t even notice them until it is too late.

The Unmeasurable Moments

Life is full of things we can measure: time, money, deadlines, productivity. But the moments that truly matter, the ones that make life worth living, are the ones that can’t be quantified. Quality time with loved ones. The graduation of your child. The fresh air on the beach. A warm hug.

I heard Jimmy Carr say something that resonated deeply with me:

“Trade the measurable with the unmeasurable.”

It’s a simple idea but incredibly profound. Nobody lies on their deathbed wishing they’d spent more time at the office or earned a little more money. What we wish for are more moments with the people we love, more experiences that fill our hearts rather than our bank accounts.

The Balance Myth

Everyone talks about balance. But what the heck is that? I think you should not completely ignore measurable things like business goals, financial success, or daily tasks. The balance is about being in a position where you can make the choices you truly want to.

If you’re building a business, it should be something that serves you and aligns with what you love. If you hate your business, it’s important to remember that the architect of that business is you. The good news? Architects can redesign.

And don’t panic. If you realize your focus or your needs have changed, that’s okay. It’s perfectly fine to:

- Redesign the business to better fit your current goals.

- Be ready to sell it and work on making that happen

- Even close it entirely, if that’s what serves you best.

My Three Quick Questions for You

- What measurable things in your life could you trade for the unmeasurable?

- Are you building a life and business you truly love or are you stuck in something you’ve outgrown?

- What’s your “one more time,” and are you making space for it?

– Rickard

Welcome To The Tax Game

Imagine you’re at a poker table playing Texas Hold’em. There are three players:

- Player 1 knows the rules, plays cautiously, folds on bad hands, and bets smartly when holding strong cards.

- Player 2 plays aggressively, bluffing occasionally but sticking to a clear strategy.

- Player 3, however, folds pocket aces (the best starting hand) and bets heavily on weak cards.

Everyone at the table is confused. Player 3’s moves seem irrational. Throwing away winning hands and wasting chips on hopeless ones. But here’s the truth: Player 3 doesn’t actually know the rules of poker. Player 3 is actually great at playing Uno but it does not help at this table. They’re not stupid, they just don’t understand how the game works.

Now, imagine the other players are speaking a language you don’t know, like Chinese. You however make a lot of words and laugh randomly. To them, your strange sounds might seem just as foolish. But the problem isn’t you, it’s that you’re trying to play without knowing the rules or the language.

This is exactly how most people approach taxes and financial systems. They’re trying to navigate a high-stakes game without understanding the rules, leading to poor decisions and lost opportunities. Let’s change that.

The Players in the Tax Game

The tax system is much like the poker table. To succeed, you must understand the players:

- The Government

- Role: Rule setter and enforcer.

- Goal: Collect revenue while incentivizing behaviors that benefit the economy and society.

- Businesses and Individuals (You!)

- Role: Active participants.

- Goal: Maximize value (profits, income, and savings) while minimizing costs (taxes, compliance efforts).

- Stakeholders (Society, Competitors, Investors, etc.)

- Role: Observers and influencers.

- Goal: Shape the environment and influence how rules evolve.

The Rules of the Game

Taxes and financial regulations are the language of this game. If you don’t understand them, it’s like being at the poker table without knowing the difference between a full house and a bluff. Key rules to keep in mind:

- Governments create rules to incentivize behavior.

Tax breaks for green energy investments or small businesses are designed to encourage actions that align with public policy goals. - The game is always changing.

Tax laws evolve with political, social, and economic shifts. Staying current is critical. - Success requires strategy.

Winning players don’t just comply, they optimize, using the rules to their advantage.

Why People Lose the Tax Game

Many people are like Player 3 in poker not because they’re incapable but because they don’t understand the rules. Here’s how this plays out:

- Folding on Winning Hands:

Missing out on deductions, credits, or incentives they qualify for, leaving money on the table. - Betting on Weak Cards:

Making financial decisions without considering tax implications, like selling investments at the wrong time or ignoring tax-efficient savings options. - Not Knowing When to Call:

Failing to act strategically when opportunities arise, like deferring income to a lower-tax year or reinvesting profits into tax-advantaged projects.

Designing Your Winning Strategy

To win the tax game it’s about playing smarter within them, not bending them. Here’s how to design a strategy that works:

Step 1: Educate Yourself

The first step to mastering the game is understanding the rules. The fastest way to do this is by finding a mentor, someone who knows the system and can guide you. Ask your network for recommendations before turning to a random online search. While self-education is an option, it’s often inconsistent and time-consuming, and you risk focusing on things that aren’t relevant to your situation.

Step 2: Make a Game Plan

Work with your mentor to create a customized game plan. This should include:

- Identifying key opportunities in your tax situation.

- Setting goals for minimizing liabilities and maximizing benefits.

- Preparing for future changes in the rules.

Step 3: Implement Your Strategy

Once your plan is set, take action. Execute the steps outlined by your mentor and track your progress. Regularly review and adjust as needed to stay aligned with your goals.

Bonus Step: Help Someone Else

If you find success, extend a hand to another entrepreneur or individual. Teach them how to play the game better. The more players who understand the rules and play strategically, the more rewarding and fun the game becomes for everyone.

Just like in poker, ignoring the rules of taxes and financial systems leads to predictable consequences:

- Penalties and Fines:

Missteps can result in audits, back taxes, and hefty penalties that drain your resources. - Missed Opportunities:

Failing to use tax-efficient strategies leaves money on the table that could have been reinvested into your life or business. - Increased Stress:

Operating without a strategy is exhausting and unsustainable. Knowledge and planning bring clarity and control.

When you educate yourself, create a plan, and implement it strategically, you stop being a passive participant and start winning.

3 Quick Questions to Get Started:

- Are you fully aware of the tax rules that apply to your situation?

- Do you have a mentor or advisor helping you navigate the system?

- What’s one step you can take today to optimize your strategy like reviewing deductions or asking for professional advice?

One thing I think is important is that the tax game isn’t about outsmarting others.

It’s about playing a better game with the tools it gives you.

Master the rules, play with purpose, and design your winning strategy.

And like Simon Sinek put it, this is not a single game you play once but an infinite game and if we know we will play this a long time I think we want to have fun doing it.

Rickard

Ps. Full disclaimer. I am by no means a tax guru of any sort and don’t claim to know how to play this game the best way at all. If we were playing Poker I am still at the level of playing Uno.

Is The Zeigarnik Effect Stopping You?

Do you find yourself constantly jumping from one project to another, always chasing the latest idea or trend, yet never feeling truly satisfied? If so, you’re not alone. This perpetual pursuit can be a sign of not closing off projects or unresolved conflicts in your life.

The Cycle of Unfinished Business

Many people identify as either project starters or closers. Starters are full of enthusiasm at the beginning but often struggle to see things through to the end. While it’s great to have the spark of initiation, without the skill of closing, distractions accumulate, and no project ever truly launches.

Why Learning to Close Matters

I believe that anyone who is a starter needs to learn the skill of closing. By facing the tough stuff and practicing the art of completion, you not only finish more projects but also gain a deeper sense of satisfaction. Closing off projects frees up mental space and energy, allowing you to focus more effectively on new endeavors. (You have probably heard about the 3 min rule? If something takes less than 3 min, instead of planning it, just do it.)

My Own Struggle with Unfinished Projects

I know this from personal experience. I’ve bought courses, subscribed to services, and initiated projects that I never got around to completing. Right now, I still have some open loops I’m working to close and what brings me to write about this topic. What helps me is the accountability of a mentor and coach. They motivate me and push me through the uncomfortable phases, ensuring I don’t abandon what’s important.

Zeigarnik Effect – The Psychological Effect at Play

This tendency to remember and be affected by unfinished tasks is known as the Zeigarnik Effect, a psychological phenomenon identified by psychologist Bluma Zeigarnik. It suggests that incomplete tasks linger in our minds, causing mental tension and distraction. By closing these tasks, we alleviate this tension and gain a sense of accomplishment.

Elon Musks Super Power

If you’re tired of feeling unsatisfied and always chasing the next new thing, consider focusing on closing off your current projects before taking on a new one.

Learn to say “no” is one of the super powers that Elon Musk has been titled with. He says “no” very often because it bring him away from a bigger “yes” (flying to Mars).

Practice facing the challenging parts head-on. You’ll not only complete more projects but also find greater fulfillment in your work and personal life.

If this resonated with you, I’d love to hear your thoughts. Send me a message on Instagram @rickardlong, and let’s continue the conversation.

Quick 3 Questions

- What unfinished project can you commit to completing this week?

- How could having a mentor or accountability partner help you stay accountable and motivated?

- What steps can you take to improve your ability to close projects and reduce distractions?

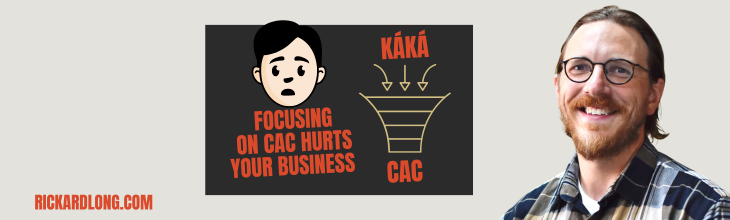

Is CAC irrelevant?

As business owners and entrepreneurs, we often find ourselves obsessed with reducing Customer Acquisition Cost (CAC). The logic seems sound: the less it costs to acquire a customer, the better for our bottom line. But what if this fixation on lowering CAC is actually hindering our growth and profitability?

After listening to the Chief Marketing Officer of Revolut, Antoine Le Nel, it occurred to me instead of relentlessly chasing a lower CAC, it’s time to shift our focus to Return on Investment (ROI) and Customer Lifetime Value (LTV). By doing so, we not only consider the cost of acquiring a customer but also the revenue and profit they bring over time.

Obsessing Over CAC – The Downside

Reducing CAC can indeed bring in more customers at a lower upfront cost. However, a sole focus on CAC can lead to unintended consequences:

- Attracting the Wrong Customers: Lowering CAC might mean targeting a broader audience that isn’t the ideal fit for your product or service. These customers may not stay long or engage deeply with your offerings.

- Compromising on Quality: Cutting costs in acquisition efforts can reduce the effectiveness of your marketing strategies, leading to lower-quality leads.

- Short-Term Gains, Long-Term Losses: A low CAC doesn’t guarantee profitability if the customers acquired don’t contribute significantly over time.

Why ROI and LTV Matter More

- Quality Over Quantity: Focusing on ROI ensures that your marketing efforts generate profitable returns. It’s not just about how many customers you acquire, but how valuable they are to your business.

- Sustainable Growth: LTV measures the total revenue a customer is expected to generate over their lifetime with your company. By maximizing LTV, you foster long-term relationships that contribute to sustained profitability.

- Informed Decision-Making: Prioritizing ROI and LTV provides a more comprehensive view of your business health, allowing for smarter investments in marketing and customer retention strategies.

Balancing CAC with ROI and LTV

This isn’t to say that CAC should be ignored. Instead, it should be balanced with ROI and LTV:

- Calculate the Ratio: Use the LTVratio to assess the efficiency of your acquisition strategies. A higher ratio indicates that the value of customers outweighs the cost of acquiring them.

- Segment Your Customers: Identify which customer segments have the highest LTV and focus your acquisition efforts there, even if the CAC is higher.

- Invest in Retention: Allocate resources not just to acquire new customers but to retain existing ones, thereby increasing LTV.

Action Steps

- Analyze Your Metrics: Start by thoroughly understanding your current CAC, ROI, and LTV. Identify trends and areas for improvement.

- Refine Your Target Audience: Focus on attracting customers who are the best fit for your product or service, even if it means a higher CAC.

- Enhance Customer Experience: Invest in quality customer service and support to increase satisfaction and loyalty.

- Leverage Upselling and Cross-Selling: Introduce complementary products or services to increase the value each customer brings.

- Monitor and Adjust: Continuously track these metrics and adjust your strategies accordingly.

Quick 3 Questions

- Are you attracting the right customers who will provide the highest LTV, even if it means a higher CAC?

- How can you enhance your product or service to increase customer satisfaction and ROI?

- What strategies can you implement today to balance CAC with a stronger focus on ROI and LTV?

—Rickard

This this help you? Feel free to reach out to me over instagram https://www.instagram.com/rickardlong/

Feel Stagnant? Do this!

In 2023 I had the feeling that my business was on a good path but I also knew I had to figure out what the future vision for the business should be.

As business owners, we often get caught up in the day-to-day operations, making it challenging to step back and see the bigger picture. And I was a bit stuck in my current state and needed to widen my view. So I used this question:

“What would someone change on the first day or within the first year if they took over my business?”

This question forces you to view your business through fresh eyes, identifying areas that may have been overlooked or deemed “good enough” under your leadership. A new owner would likely scrutinize every aspect, from operations and finances to marketing and team dynamics, seeking immediate improvements to maximise success. It is of course similar to the principles that many use when a business wants to scale or sell, as written in the book “Build to Sell”.

Why This Question Matters

- Identifying Blind Spots: We all have biases and blind spots. A new perspective can highlight inefficiencies or outdated practices that you’ve grown accustomed to.

- Challenging the Status Quo: Complacency is the enemy of growth. Questioning existing processes can lead to innovative solutions and improvements.

- Focusing on High-Impact Areas: A new owner would prioritize changes that offer the greatest return on investment. This can help you realign your efforts toward what truly drives your business forward. For me I quickly made the decision to cut out some of the events we were doing that were not replicable and did not show any benefit to the majority of our customers.

Implementing the Insight

- Conduct an Internal Audit: Objectively assess each area of your business. Where are the bottlenecks? What feedback have you been ignoring?

- Seek External Opinions: Sometimes, an outsider’s perspective can provide invaluable insights. Consider hiring a consultant or discussing with a mentor which I do on a weekly basis on small or big matters.

- Develop an Action Plan: Identify the top changes that could have the most significant impact and create a strategic plan to implement them over the next year.

The Most Important Strategy for Next Year

By adopting the mindset of a new owner, you’re positioning yourself to do the things you might be procrastinating that would lead to impactful changes. This approach could very well be the most important strategy you implement next year. It encourages continuous improvement, adaptability, and a focus on what is most important which leads to growth. Stephen Covey wrote in his book “7 Habits of highly successful people” about the principle of putting first things first and I like this quote:

“Never let something that is of less importance come in front of the most important things”

Quick 3 Questions

- What immediate changes would a new owner prioritize in your business, and why haven’t you addressed them yet?

- How can you objectively evaluate your business operations to uncover hidden inefficiencies or opportunities for growth?

- Who can provide you with an unbiased perspective on your business, and how soon can you engage with them to start this transformative process?

—Rickard

How to beat Starbuck

How can a business with no sales department expand to more locations and grow faster than Starbucks?

Greg Glassman, the founder of CrossFit, often said they never had a marketing or sales department. People came to them because they wanted to be part of what CrossFit offered. Instead of traditional sales tactics, they had a committee to review applications from prospective affiliates.

The selection process was simple yet profound. Applicants who expressed a genuine mission to help people got the green light. Those who touted their MBA degrees or claimed to have a unique business model were often declined. Glassman knew that the only way to succeed with a small gym was to be entirely client-centric starting and ending with the client’s needs.

The success of CrossFit boiled down to two key elements:

- A Great Product: CrossFit delivered results like no other. The workouts were effective, the community was supportive, and the transformations were real. This made people naturally enthusiastic about sharing their experiences.

- Authentic Storytelling: CrossFit produced media that shared genuine stories from clients, gyms, and athletes. These videos garnered millions of views because they showcased real proof of the product’s impact. They were rough. They did not look like commercials. The stories resonated because they were honest and relatable.

Most affiliate buyers were individuals who had experienced their own transformation through CrossFit. The product was so compelling that it inspired people to become part of the mission themselves.

The Takeaway

Marketing doesn’t always require a massive budget or a dedicated department. Sometimes, it simply requires an exceptional product and authentic stories that resonate with people. When your service genuinely helps others, they will become your most powerful advocates.

Quick 3 Questions

- Is your product or service so good that people can’t help but talk about it?

- Is it so authentic and impactful that you could bring in a camera at any time and capture compelling stories?

- Are you genuinely starting from the client’s perspective and focusing on their needs?

Breaking the Cycle of Self-Sabotage

As entrepreneurs and business owners, we often find ourselves trapped in cycles of self-sabotage. We dream big, set ambitious goals, but somewhere along the way, we hit a wall, not because of external obstacles, but because of the barriers we create for ourselves.

I’ve been there, and I often catch myself being there. I’ve blamed taxes, the market, even my own team for the lack of growth in my business. But the hard truth is, the biggest obstacle was me.

The Ego Trap

Our ego can be a double-edged sword. On one hand, it drives us to achieve; on the other, it can blind us to our own shortcomings. Admitting that we don’t have all the answers is tough. It feels vulnerable. But acknowledging our limitations is the first step toward growth. If you’re constantly telling yourself that everything is fine when it’s not, you’re letting your ego hinder your progress.

Fear: The Silent Killer of Dreams

Fear manifests in many ways—fear of failure, fear of rejection, fear of the unknown. It can paralyze us, making us stick to what’s comfortable rather than what’s necessary. I remember hesitating to implement new strategies because I was afraid they wouldn’t work. That fear cost me time and opportunities. If you’re scared, consider seeking guidance from a coach or mentor who can help you navigate through the uncertainty.

Blame Game

It’s easy to point fingers when things go wrong. Taxes are too high. The team isn’t performing. The economy is sluggish. While these factors can impact your business, fixating on them diverts attention from what you can control. If taxes are eating into your profits, revisit your pricing strategy. If your team isn’t meeting expectations, perhaps it’s time to improve your delegation skills or invest in training.

The Game of Business

Think of business as a game with established rules. These rules include market dynamics, customer behavior, financial principles, and yes, taxes. You can’t change the rules, but you can change how you play the game. Learn the rules inside out, and strategize accordingly. If you’re unsure how to proceed, don’t try to reinvent the wheel. Reach out to someone who has walked the path before you.

Ownership and Responsibility

One of the most empowering realizations I’ve had is that I am responsible for everything that happens in my business. If I don’t have enough time, it’s because I haven’t prioritized effectively. If there are problems, it’s because I’ve allowed them to persist. Taking full ownership isn’t about self-blame; it’s about recognizing the power you have to effect change.

Breaking Free

To break the cycle of self-sabotage, we must first recognize it. Be honest with yourself about the state of your business. Reflect on your actions and attitudes that may be holding you back. It’s not an easy process, but it’s a necessary one for anyone serious about growth.

3Qs to Propel You Forward

- What is one area in your business where you’ve been placing blame externally, and how can you take ownership to change it?

- Who can you reach out to for guidance, a mentor, coach, or peer, who has successfully overcome the challenges you’re facing?

- What is one fear that’s been holding you back, and what actionable step can you take this week to confront it?

Remember, the journey of entrepreneurship is as much about personal growth as it is about business success. By addressing the internal barriers, we pave the way for external achievements.

Rickard

Why Repeat Customers Are the Lifeblood of Your Business

One of the most important metrics to track in any business is customer retention. A happy customer returning to make a repeat purchase is more than just a sale, it’s their way of casting a vote for your business. If you’ve done a great job, your customers will come back. If they don’t, then there’s an opportunity for growth you’re missing.

I recently spoke to a hotel owner who told me that most of her guests didn’t return after their first stay. This is especially challenging in the hotel industry, where it can be difficult to generate repeat business.

But as we talked, it became clear that the issue wasn’t the service or the location, there was no system in place to make rebooking easy or encourage repeat visits. The hotel was listed on platforms like Airbnb and Booking.com, making it more of a commodity where guests often book simply because it was the only available option, or the cheapest.

The hotel had numerous unique selling points (USPs) that could set it apart, and these could be highlighted in a way that encouraged loyalty. With no loyalty program, follow-up emails, or easy rebooking systems, the guests don’t have a reason to return. In contrast, large hotel chains have loyalty programs and automated systems that make it easy to rebook, incentivizing guests to stay within their brand.

For smaller businesses, the lesson is clear: repeating sales is not only about offering a good product or service; it’s about building relationships, creating systems, and making it easy for customers to return.

In Two-Brain Business, the concept of customer retention is captured through something called “LEG” (Length of Engagement). This measures how long a customer stays committed to your service and is a key indicator of business health.

The longer the LEG, the more successful your business is likely to be. I’ve learned a lot from my work with TwoBrain, where we emphasize that this is a well-known but often neglected metric. Creating systems and incentives to nurture customer loyalty will not only drive growth but create long-term stability for your business.

3 Quick Questions (3QQ) to Ask Yourself:

- Do you have a system in place that makes it easy for your customers to make a repeat purchase?

- Are you offering incentives (like loyalty programs or offers) for customers who come back?

- Are you making it clear to your customers why they should choose you again over the competition?

At the end of the day, your repeat customers are your biggest fans. It’s their return that signals the true strength of your business.

Rickard

“1000 Songs in your pocket”

In the world of business, the difference between success and failure often lies in how we communicate value. One of the best examples of this is how Apple introduced the iPod. They didn’t just list the features, like “5 GB storage.” Instead, they framed it in a way that made sense to people: “1000 songs in your pocket.” Simple, clear, and relatable.

This focus on results over features is why businesses like Apple thrive. They make it easy to understand the value of their product. You don’t have to be a tech expert to know that carrying around your entire music collection is life-changing.

So, how does this apply to gyms?

Gym owners often fall into the trap of marketing equipment or class availability. But what really matters to your clients is what those features will do for them. Here are some examples of how to position your gym to focus on results, not features:

- Feature: “We have 10 rowing machines.”

Better: “You’ll build stamina and shed pounds in half the time.” - Feature: “We offer a variety of classes.”

Better: “Transform your body and mind with workouts that fit your life.” - Feature: “We have a fully equipped strength training area.”

Better: “Feel stronger, look better, and live healthier with our personalized strength programs.”

To take this approach one step further, gather data from your clients’ results and share it. For example, track progress, share testimonials, and highlight the changes they’ve made in their health. Just like Apple, you’ll make it easy for prospective clients to see what’s possible for them.

When your gym becomes more about the transformation than the equipment, you’re no longer selling a service…YOU’RE SELLING A SOLUTION.

That’s where the real value lies, and that’s what will help you stand out.

This is how you can charge 10x more than your competitors.

QUICK ACTIONS

Here are three quick, actionable questions for entrepreneurs to gain better clarity:

- What problem am I solving for my clients, and how does it improve their life?

- Action: Write down the tangible outcomes your product or service delivers, not just its features.

- How easy is it for my clients to understand the value I provide?

- Action: Revisit your messaging. If it’s full of jargon or overly complex, simplify it to one sentence anyone can understand.

- What metrics am I tracking to show that my solution is working?

- Action: Choose 1-2 key performance indicators (KPIs) that directly reflect the results your clients get from using your service. Then, make those results part of your marketing.